The Bank of Canada needs to get serious about inflation

The Bank of Canada needs to get serious about inflation

Even though inflation is a "global problem," our inflation problem is made in Canada, by the Bank of Canada, and the solution lies at home.

My latest op-ed, in Canada’s Financial Post, is adapted from my testimony before the House of Commons Standing Committee on Finance on March 21, 2022.

The op-ed may be found here on the FP website and is print in Canada today.

The piece is pasted below for your convenience. The version below, the final version as filed, differs slightly from the published version, due to minor copy edits before going to press.

The Bank of Canada needs to get serious about inflation

The problem inflation poses is real, pressing and getting worse

Vivek Dehejia

During last fall’s election campaign, while the Bank of Canada’s mandate was under review, Prime Minister Justin Trudeau made the perplexing claim that he “doesn’t think about monetary policy.” Even so, his re-elected government renewed the central bank’s inflation target at the two per cent midpoint of a one to three per cent band. Last week’s release of February’s CPI data tell us inflation is now running at 5.7 per cent. That’s the highest we’ve seen it since the early 1990s, and it’s rising. The problem it poses is real, pressing and getting worse.

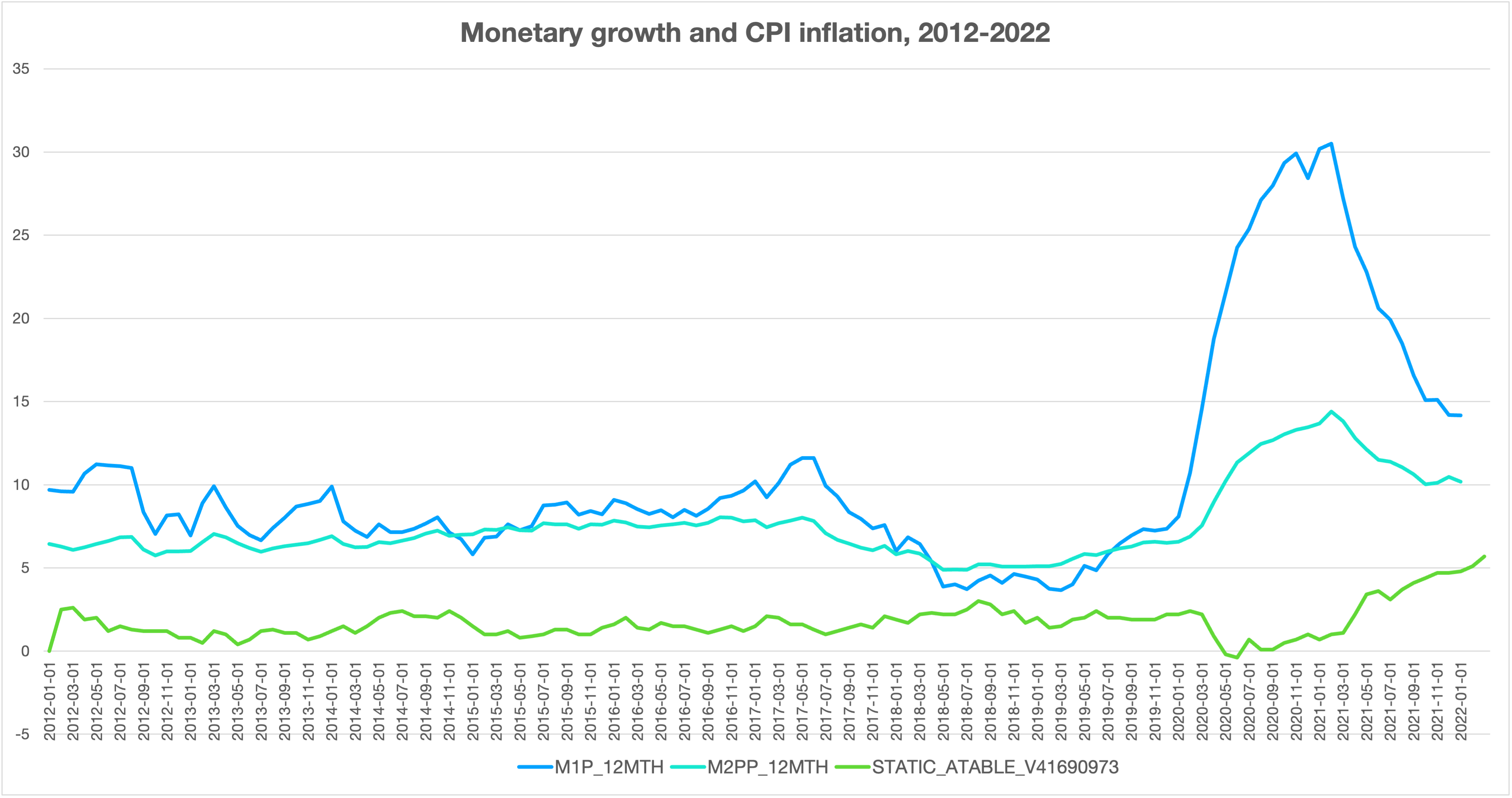

The usual line from the government is that inflation is a “global problem.” It is true that most advanced economies are experiencing rising prices. But that’s because they have all been following the same hyper-expansionary policies. Our own inflation is a creation of the Bank of Canada. The chart shows CPI inflation and narrow and broad definitions of money (M1+ and M2++) for the last ten years. After remaining steady for much of this period, they began creeping up in the middle of 2019, and have since grown explosively as part of the concerted effort by the government and the central bank to ward off the detrimental effects of the COVID19 pandemic. Although their growth has tapered off, these aggregates keep increasing at extraordinary rates. For example, M1+, defined as currency held by the public and all chequable deposits at financial institutions, is still growing at a jaw-dropping 14 per cent, year-on-year.

To put this in perspective: to maintain an inflation rate around two per cent, and to allow a bit of a margin to prevent deflation, which presents its own challenges, the money supply should be growing at no more than five to six per cent per year. We are way above that. Meanwhile, the current policy interest rate is at just 0.5 per cent, well below even the most conservative estimates of the “neutral” rate — that consistent with full employment and stable inflation. The Bank of Canada puts this neutral rate at 1.75 to 2.75 per cent — which means monetary policy is highly inflationary at present.

South of the border, after hedging its bets for the last year, the U.S. Federal Reserve has begun an aggressive move to raise rates. Last week, the Federal Open Market Committee, the Fed’s policymaking body, raised the policy rate to 0.5 per cent, and it has promised seven more rate hikes, with the goal of getting to 2.8 per cent by late next year. Fed Chairman Jerome Powell has said he is “acutely aware of the need to return the economy to price stability and determined to use our tools to do exactly that.”

That U.S. inflation is running hotter than ours, at 7.9 per cent, is no reason for complacency here in Canada. Unfortunately, Bank of Canada Governor Tiff Macklem was vague in his comments March 3 before the House of Commons Standing Committee on Finance. Commenting on the previous day’s rate hike, he made no specific commitment regarding future rate hikes; nor did he commit to ending quantitative easing, which would involve moving into a phase of disinvestment, where the Bank of Canada’s balance sheet begins to shrink.

Governor Macklem did conclude his remarks by saying “the Bank is determined to control inflation.” But it is hard to understand how the Bank of Canada proposes to control inflation and meet its inflation target with a policy stance that is still inflationary by any measure. The danger of moving too slowly is that high inflation gets baked into people’s expectations, thereby setting up a damaging “wage-price spiral” reminiscent of the “stagflation” that hit most advanced economies, including the U.S. and Canada, in the 1970s.

Canada had a more recent bout of high and persistent inflation in the late 1980s and early 1990s, which was only tamed by double-digit interest rates under then-Governor John Crow. The unfortunate side effect was an overvalued dollar, which exacerbated the temporary, but necessary, recession the disinflation created. Crow was widely pilloried for the hardship his policy caused, but he had the moral support of then-Prime Minister Brian Mulroney, and the disinflation succeeded. The tough medicine allowed a re-anchoring of the public’s expectations, thus setting up our current era of two per cent inflation targeting.

Today, no less than in the late 1980s, there is no room for complacency. The Bank of Canada needs to get serious about reducing inflation and the Trudeau government needs to get behind it.

Vivek Dehejia teaches economics at Carleton University. This is adapted from his recent testimony before the House of Commons Standing Committee on Finance.

CHART

The chart shows growth in the narrowest and broadest monetary aggregates and CPI inflation. The data is sourced from the Bank of Canada website. The dark blue line is M1+, a narrow measure of the money supply; the light blue line is M2++, a broad measure of the money supply; and the green line is CPI inflation.